menu

In all the world there is no one quite like you – you are unique. God made you to fill a special place in His Kingdom. As a one-of-a-kind individual (or family), your estate planning and generosity desires are also unique.

Your plans and gifts will be like none other –you don’t have to settle for cookie-cutter solutions. To help you achieve stewardship success in your estate and gift design, we offer a variety of services – each one guided by Biblical principles and time-proven, tax-advantaged strategies. Each one can help you discover God’s unique plan of stewardship for you.

You can explore these principles and strategies by selecting one of the buttons below. If we can help you achieve your stewardship goals –our services are provided without cost or obligation – please contact Travis:

Scientists tell us that only about 10% of an iceberg is visible above the water’s surface. The great mass – some 90% of the iceberg is below the surface and hidden from view. Similarly, the Christian steward’s assets (or estate) are often approximately 10% in cash (liquid assets) and the remaining 90% in non-cash, non-liquid assets.

For generous stewards, this can be highly frustrating. “I’d really like to give more – but I just don’t have any more cash money…” Regardless of income, nearly everyone reaches the point of – “I can’t give away any more cash.”

Are there options for the giver who has reached their personal “cash limit?” Yes! For many, “the other 90%” of their financial assets holds the key to giving to their heart’s desire.

As a general rule – if an asset has an ascertainable value and is commonly bought and sold, it may be possible to use it to fulfill your generosity desires. However, some assets have complicated tax and ownership rules that make their use as a charitable gift less desirable or even prohibited.

Here is a partial list of non-cash assets that are commonly used to make generous charitable gifts.

Tangible Property – Physical property that can be moved.

Artwork, automobiles, boats, RVs, motorcycles, and collectibles such as jewelry and coins are all tangible items that can be used to make charitable gifts. Specific valuation and charitable deduction rules apply making each item more or less valuable as a gift for the giver. However, once converted to cash (or put to use by the ministry) – tangible items have value to accomplish the ministry purpose and mission.

Securities (Stocks, Bonds, Mutual Funds) – Simplest to give are those traded on a public stock exchange or market.

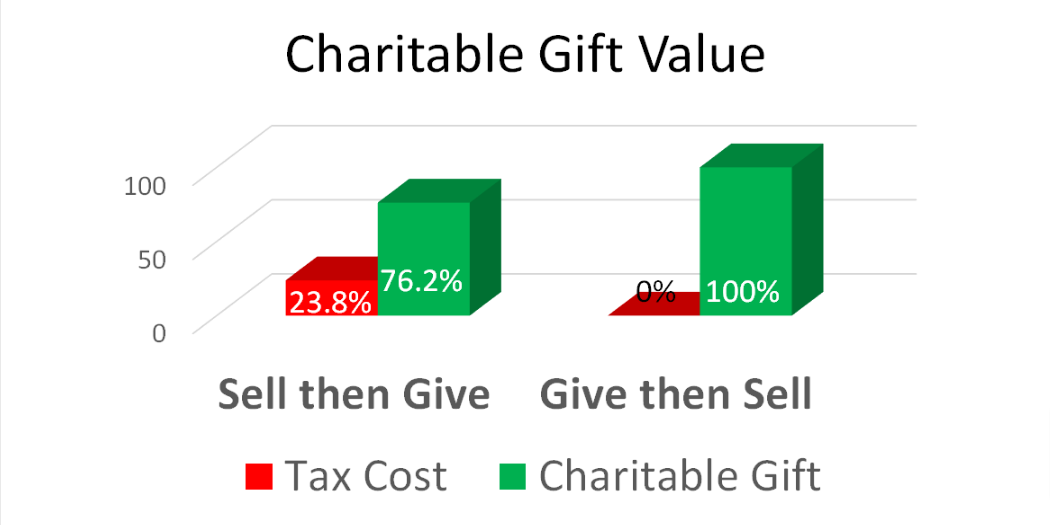

Example: Ralph and Marge have a significant portfolio of highly appreciated stock that is subject to equally significant capital gains tax if they sell it. Recently, they learned that using the stock for some of their giving to ministry might make good financial sense.

In a typical year, Ralph and Marge have been giving $5,000 to their favorite ministry. This year, however, rather than writing a check, they donated $5,000 in shares of appreciated stock. The ministry sold the shares providing cash to do their mission. For the ministry, the gift was virtually the same as past gifts from Ralph and Marge.

The results for Ralph and Marge, however, were important. Along with a charitable tax deduction for the fair market value of the donated stock, they also avoided the capital gains tax that would have been paid had they sold the stock. In addition, they can use the normally donated cash for any purpose they choose. And, of course, they still made their desired gift to their favorite ministry.

The following chart compares the value of contributing appreciated stock to charity with the result of selling the stock and then making a gift of the after-tax cash. This illustration assumes a 23.8% combined federal and state capital gains tax rate.

Closely held securities can also be used to make charitable gifts – but may require additional planning.

With all contributions of securities, it is important to consult your tax professionals to be sure you are accomplishing your generosity desires in the most cost-effective way for both you and the recipient ministry.

Individual Retirement Accounts – Commonly referred to as an IRA

Example: Ralph and Marge are in their late 70s and want to give a generous gift to their favorite ministry for the current campaign. They are doing well living on their fixed income payments and find that they really do not need the income from the required minimum distributions (RMD) they must take from their IRAs this year.

After learning of the qualified charitable distribution provision in the Tax Code – Ralph and Marge each instructed their IRA custodian to send a distribution equal to this year’s RMD directly to ministry to help with the campaign. While they will not receive a charitable tax deduction for the gift, they won’t have to claim the distribution as income – providing essentially the same tax benefit.

Ralph and Marge are planning to use the qualified charitable distribution in coming years to increase their generosity. If they find they need the RMD (or more), they will simply not request the distribution to charity retaining the income for themselves.

Generally, if you are at least 70.5 years of age, IRAs can be excellent assets for making current gifts so long as you understand and follow the withdrawal and taxation rules carefully.

The qualified charitable distribution provision in the Tax Code allows you to have your IRA custodian send a distribution directly to your chosen ministry rather than to you. Since you don’t receive the distribution, you will not have to claim it as income. Further, the distribution can count toward your RMD for the year of the distribution.

We have prepared a helpful eBook, A Guide to Charitable Giving Through Your Retirement Accounts, and you can read or download it here.

Real Estate – Buildings and Land

Example: Ralph and Marge invested in a commercial warehouse property partnership as an income-producing asset. After several years of receiving income and seeing the property grow in capital value, they determined they no longer needed the asset.

Their charitable adviser suggested that making an outright gift of the warehouse might allow them to make significant gifts to ministries they love and support. Ralph and Marge transferred their interest in the warehouse to a charitable foundation.

Ralph and Marge received a charitable tax deduction for the full appraised fair market value of the property. The property was sold, and Ralph and Marge instructed the charitable foundation to distribute the net proceeds to two of their favorite ministries who happily received the large cash distributions to further their work. Ralph and Marge enjoyed the satisfaction of excellent tax benefits and knowing they had made a lasting Kingdom impact with a gift of appreciated real estate.

Real estate gifts can be of houses, land, condominiums, vacation homes, commercial buildings, or most any type of real property. As with all non-cash gifts, tax rules vary by state, and you should consult your own tax professionals before making a gift of real estate. If you are seeking to increase your generosity, and if you own real estate – the combination may be just right to accomplish your desires.

Commodities – The most common is a gift of grain from an active farmer.

Example: Ralph and Marge farm several hundred acres of cropland. Each year during the harvest they deliver one truckload of grain to their local elevator in the name of their favorite ministry. All the paperwork they receive when delivering this load shows the ministry as owner.

Once notified that they have a load of grain in their name, the ministry orders the elevator to sell at the current per bushel price. In a few days a check for the net value of the donated grain arrives at the ministry’s office. The cash gift is then put to work accomplishing the mission that Ralph and Marge so dearly love.

Though Ralph and Marge do not receive a charitable tax deduction for the gift of the load of grain, they do receive a kind letter of acknowledgement from the ministry leader. This confirms that the grain has been sold and that the ministry is putting the net proceeds of the sale to work accomplishing the mission.

In lieu of a charitable tax deduction, Ralph and Marge get to deduct the cost of producing the grain, and do not have to realize the taxable income that the sale of the grain would have produced. The net tax impact of their commodity gift is beneficial to them.

As with all gifts of non-cash assets, the tax rules are specific, and you should consult your own tax professionals before making a gift of any commodity.

Life Insurance – Policies can be gifted to the ministry or can name the ministry as a beneficiary.

Example: When their children were young, Ralph and Marge each purchased a life insurance policy naming the other as beneficiary. The thought was that if death occurred, the surviving spouse would need the additional income to care for the family. Now that their children are grown and no longer dependent, and because they have accumulated other assets, Ralph and Marge no longer need the policies.

In considering how they might increase their charitable giving to support their favorite ministry, Ralph and Marge learned that they could gift the policies outright to the ministry. Since each policy has a cash value, the ministry can choose to either hold the policies until death or surrender them and put the cash to work doing the mission today.

Ralph and Marge will receive a charitable tax deduction per the rules of life insurance contributions and know that they are making a significant gift to the ministry right now. If they choose, they can also make annual gifts of cash to the ministry that will be used to pay any ongoing premium – and receive further charitable tax deductions for their cash gifts.

If you have life insurance policies that are no longer needed for their original purpose – consider with your agent, the possibility of making a gift to ministry. You may find your policy is a perfect tool for increasing your generosity desires.

We have prepared a helpful eBook, A Steward’s Consideration of Life Insurance, which you can read or download here.

When you desire to increase your generosity – consider “the other 90%” – your non-cash assets.

May we help? We have many resources available and can produce specific illustrations to explain how non-cash asset gifts can work for you.

Please contact us today!

Ralph and Marge have entered into their retirement years and are prayerfully considering the stewardship of all of their assets – often referred to as their estate. While they live comfortably and have considered making gifts of some “extra” assets (mostly CDs and a few low-dividend stocks), they wonder if they might someday need the income these assets can provide.

Are there charitable options for Ralph and Marge that could allow them to both receive income and make a generous gift? Yes! Here are two options.

The Charitable Gift Annuity (CGA)

Like all annuities, the CGA provides income based upon the age(s) of the annuitant(s). The older you are, the higher the income paid.

Benefits of the CGA include fixed income for life (a portion may be tax-free), a charitable tax deduction, partial avoidance of any capital gains tax, and the joy of knowing you are making an important contribution to Kingdom ministry.

The charitable gift annuity is an agreement between you and a specific charity. They are most typically funded with cash and/or appreciated securities. The following chart represents a sample of current CGA rates for one and two life annuities.

| Single Life Age | % Rate | Two Lives Ages | % Rate |

|---|---|---|---|

| 65 | 5.7 | 65/68 | 5.1 |

| 68 | 6.1 | 70/72 | 5.6 |

| 72 | 6.6 | 73/75 | 6.0 |

| 75 | 7.0 | 78/80 | 6.8 |

| 80 | 8.1 | 83/85 | 7.8 |

| 85 | 9.1 | 85/88 | 8.5 |

To learn more about charitable gift annuities, you can read or download our eBook, A Guide to Charitable Gift Annuities, here.

The Charitable Remainder Trust (CRT)

Example: Several years ago, Ralph and Marge decided to move across town, and they purchased a new house. Rather than sell their old house, they decided to keep it as a rental property. This worked quite well until Ralph passed away and Marge was left to manage the property rental and maintenance.

Because she didn’t enjoy “fixing broken toilets,” Marge looked for another option. A charitable gift planner at her favorite ministry explained how Marge could give the rental house to a Charitable Remainder Trust, receive income for life from the trust, and not have to manage the rental property.

After further exploration, Marge learned that she would also receive a charitable tax deduction and that her favorite ministry would receive a cash distribution at her death. All-in-all, the concept made good sense to Marge, and she is now enjoying income similar to the rent – without ever having to fix another broken toilet!

The CRT has many of the same benefits of the CGA – but can be more flexible for the giver(s). With a CRT you can choose to receive fixed or variable income depending upon your needs and desires. CRTs can be funded with cash, appreciated securities, or other non-cash, non-liquid assets. While CGAs are generally most advantageous for older individuals, the CRT may work for much younger adults as well.

Because the CRT is a separate tax-filing entity, it is most useful for those looking to contribute at least $100,000. If you want a more hands-on agreement, or want to use a non-cash, non-liquid asset to produce lifetime income and make a generous gift, the CRT may work well for you.

You can read or download our eBook, A Guide to Charitable Income Agreements, here.

Ralph’s family was, on the surface at least, cordial to one another – some would even say loving, caring and kind. Until…

Until Ralph died and during his estate settlement, the old adage of “everything changes when there’s money on the table,” proved true. Ralph’s children disagreed on how his estate should be distributed – disagreements turned into disappointment and bitterness. For years after his passing, Ralph’s family remained estranged from one another.

Is family discord absolutely unavoidable when settling a deceased family member’s estate? No, but as Christian stewards, our first task is to determine God’s plan of stewardship for our estate. God’s word contains principles that give us guidance, and by following them, we can recognize and address potential areas of family conflict.

4 Steps to Estate Planning Stewardship Success

May we help you review or create an estate plan that can meet your needs, provide for your family and favorite ministries -- and honor the principles God has given in His word?

We have prepared a practical workbook, Your Estate Planning Guide, which you can download here, to help you gather the personal information you will need for your planning process. Or if you would like to speak with someone regarding your unique situation – please contact us today.

The Charitable Remainder Trust (CRT)

Example: Several years ago, Ralph and Marge decided to move across town, and they purchased a new house. Rather than sell their old house, they decided to keep it as a rental property. This worked quite well until Ralph passed away and Marge was left to manage the property rental and maintenance.

Because she didn’t enjoy “fixing broken toilets,” Marge looked for another option. A charitable gift planner at her favorite ministry explained how Marge could give the rental house to a Charitable Remainder Trust, receive income for life from the trust, and not have to manage the rental property.

After further exploration, Marge learned that she would also receive a charitable tax deduction and that her favorite ministry would receive a cash distribution at her death. All-in-all, the concept made good sense to Marge, and she is now enjoying income similar to the rent – without ever having to fix another broken toilet!

The CRT has many of the same benefits of the CGA – but can be more flexible for the giver(s). With a CRT you can choose to receive fixed or variable income depending upon your needs and desires. CRTs can be funded with cash, appreciated securities, or other non-cash, non-liquid assets. While CGAs are generally most advantageous for older individuals, the CRT may work for much younger adults as well.

Because the CRT is a separate tax-filing entity, it is most useful for those looking to contribute at least $100,000. If you want a more hands-on agreement, or want to use a non-cash, non-liquid asset to produce lifetime income and make a generous gift, the CRT may work well for you.

You can read or download our eBook, A Guide to Charitable Income Agreements, here.

Planning Tools for Christian Stewards

Wills and Revocable Living Trusts – are often considered the foundational documents for estate planning and distribution.

A Will is a document that expresses the final distribution desires of an individual. Wills are subject to state law and nearly always require the involvement of the probate court. A Will distributes only property that was titled solely in the name of the deceased.

A Revocable Living Trust can be used by an individual or a couple. The Trust provides management of assets during lifetime and final distributions at death. It will avoid the probate process on assets that are titled to the trust during lifetime.

Powers of Attorney – give another individual the legal ability to make decisions on your behalf. They are important when an individual is disabled and cannot manage their business and/or medical affairs.

Titling – must be coordinated with your legal documents to assure that your planning desires are accomplished. Titling can be a very useful way to transfer assets, or it can be the “fly in the ointment” that creates havoc in your plans.

Beneficiary Designations – can often be used to transfer assets with minimal cost and delay. Some assets, like life insurance and qualified retirement accounts, have built-in beneficiary arrangements. Many other financial instruments and tangible assets can also be transferred, without probate, by beneficiary designation.

Making Gifts From Your Estate

You can continue to give beyond your lifetime with a bequest from your estate. You can include language in your Will or Trust to make gifts to Watered Gardens Ministries. Your bequest can be:

Your attorney can help you include a gift to Watered Gardens Ministries in your estate documents. Our legal name is:

Watered Gardens Ministries, a not-for-provide organization organized in the state of Missouri, with principal offices located at 531 Kentucky Ave, Joplin, MO 64801, Federal Tax ID # 20-2586821.

You can also designate a gift today that will be completed in the future by naming Watered Gardens Ministries as a beneficiary of banking or investment accounts, life insurance retirement plan assets, and even real estate. Request the appropriate beneficiary designation forms from your account manager to complete the gift designation.

To learn more about basic tools and to help you gather the personal information you will need for the planning process, download Your Estate Planning Guide here.

Copyright © 2026 Watered Gardens